Happy NAFTA weekend!

On December 17th, 1994, Mexico, Canada, and the USA signed the North American Free Trade Agreement. No more extra taxes slapped onto (each other’s) imported goods just for the fun of it – no longer would the citizens of each country have to pay artificially inflated prices for grocery items from across the border. Red tape would die an ignoble death, and the combined surface area of Mexico, the USA, and Canada (that is, in short, the whole landmass of North America) would be one free open trade zone of economic prosperity.

Was the idea.

Yet Ross Perot, 1994’s infamously unexpected presidential candidate (whose potential win we have both analysed and spoofed), was vehemently against the idea.

“You implement that NAFTA, the Mexican trade agreement, where they pay people a dollar an hour, have no health care, no retirement, no pollution controls, and you’re going to hear a giant sucking sound of jobs being pulled out of this country.”

Ross Perot, 2nd Presidential Debate, 1994

Unlimited free trade would move jobs where labor was cheapest (Mexico), in conditions the US itself would not countenance, and ruin the good jobs and arrangements that already existed between US workers and their companies. He feared that rather than increasing American purchasing power, NAFTA would wipe out their earnings.

The demise of American manufacturing has been a powerful political undercurrent of the 21st century. The resentment, bitterness and despair of such total destruction of livelihood came to the forefront with Trump. He explicitly blamed NAFTA, positioning himself against free trade and for more protectionist, nativist policy.

But did either Perot’s predictions or Trump’s take ever come to pass?

Here I’m essentially presenting my best understanding of other people’s research. Unfortunately for economic data, the world never sits still, and trying to pick out the consequences of one policy are difficult, but multiple people have attempted to wade through the confounders and give their best estimates. All credit to them.

First confusing the issue is that Mexico swung into an entirely unrelated monetary fiasco before the year was out. Dec 1994, Mexico was struck by the peso crisis, and went into a recession. Unemployment exploded from 4% to 7%, an unprecedented height even the 2008 GFC did not match. Jan 31, 1995, a month after signing NAFTA, the US actually contributed USD$20 billion to bailing out Mexico; they were concerned that a reduced Mexican economy would buy fewer American products and lead to lost American jobs. (It was a massively unpopular decision at the time, but Mexico repaid the debt 3 years early and the US made $500 million off of it in interest).

But the peso crisis had one other effect: when the international value of the peso crashed, one USD bought twice as many pesos as before. Essentially, to every US buyer with undisturbed dollars in their hands, it was like all those products were suddenly 50% off. It was time to buy Mexican.

The peso crisis precipitated a boom in Mexican exports to the US, and would have done so even in a NAFTA-less world. The deal contributed probably only “about one-quarter of the total growth in [Mexican] export manufacturing jobs” https://carnegieendowment.org/2004/02/25/mexican-employment-productivity-and-income-decade-after-nafta-pub-1473. ¾ of the import increase would have occurred with or without tariffs. Only 250,000 of the 1 million new jobs were attributable to the deal.

Nor was this any skin off America’s back – American manufacturing employment had the audacity to increase post-NAFTA, from 16.85 million to 17.64 million in 1998, staying above 17 million until 2001. We have five years of stable manufacturing employment under the NAFTA agreement.

Then the US hits a slump. 27% of American manufacturing jobs are lost from 2001 to Feb 2020 (pre-pandemic).

US manufacturing employment goes from 17 million in 1999 to 11 million in 2010.

What happened in 2001? China shock.

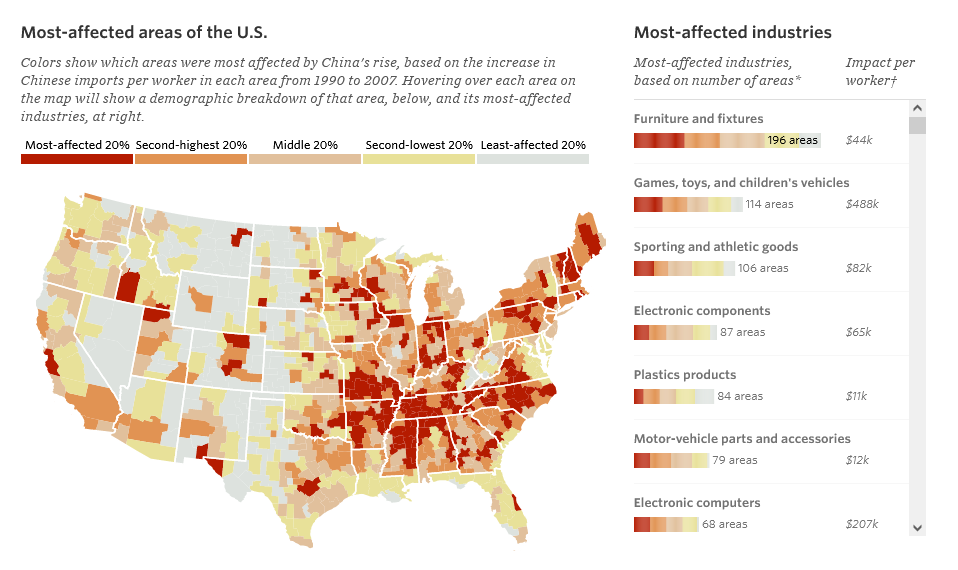

11 December 2001, China joins the WTO. In the next ten years, China shock probably took out nearly a million US manufacturing jobs; including aggregate and knock-on effects in other industries, Acemoglu et al. estimate that the US lost 2.4 million jobs in total. https://economics.mit.edu/files/9811

The original is an excellent interactive map of China’s effect on the US. While the correspondence is not particularly high, here below is the swing to Trump 2016 from 2012, if it is of interest.

Keep in mind the other value of China’s disruptive rise. In 1990, China accounted for just over one-fifth of the world’s population, and 67% of the country were living in extreme poverty. In 2015, China accounted for just under one-fifth of the world’s population, and less than 1% of the country were living in extreme poverty. It is true both that China shock has been economically and politically painful for the US, and that China’s economic surge has lifted 73.7 million people out of crippling poverty.]

The total loss in the American manufacturing industry at its lowest point (February 2010) pre-pandemic was, of course, closer to 6 million: it is not as simple as pointing a finger and blaming one country for the entire industry’s slump. China might account for a sixth of the decline and then some more associated losses, but 2000-2010 was a time of greater trade liberalization with many countries (such as India or Vietnam), who also took slices of the pie; additionally, there were massive leaps in automation from 2000-2010, which reduced employment in manufacturing.

All up, NAFTA had nothing to do with the manufacturing decline – and there’s five years’ worth of reasons to dismiss the idea that Mexico sucked jobs away from the US.

The twist to this tale is that the reverse may not be true. In Mexico’s manufacturing boom post-peso-crisis, manufacturing jobs increased by around 1.25 million – 250,000 of which was actually attributable to NAFTA. But they lost 1.3 million jobs in agriculture, where subsidized American corn had the advantage. Not all 1.3 million are directly attributable to the trade agreement, but most people seem in agreement that NAFTA is responsible for a significant chunk of those losses – easily matching the mere 250k manufacturing increase. Counterintuitively, Mexico may have lost jobs in joining NAFTA.

So while Perot was correct that free trade could drain away jobs, NAFTA was not the deal to do it, and Mexico was not a large enough entity to achieve it. That would have to wait for the continued expansion of free trade via the WTO, and the emergence of China, the economic engine that would bring a fifth of the world population into the global labour market. It would be erroneous to attribute to NAFTA a decline that only began half a decade later.

Extra reading:

- China Shock – https://chinashock.info/

- Import Competition and the Great US Employment sag of the 2000s – https://economics.mit.edu/files/9811

- Mexican Employment, Productivity and Income a Decade after NAFTA, Sandra Polaski – https://carnegieendowment.org/2004/02/25/mexican-employment-productivity-and-income-decade-after-nafta-pub-1473

- NAFTA’s Winners and Losers – https://www.investopedia.com/articles/economics/08/north-american-free-trade-agreement.asp#toc-us-manufacturing-jobs